Solar vs Fixed Deposit: Which Gives Better Returns in India (2026)?

When I visited a homeowner recently, he asked me something that made me pause.

He said:

“Why should I invest in solar?

I can just put the same money in an FD and get safe returns without any risk.”

And honestly… he wasn’t wrong.

But he also wasn’t seeing the full picture.

That one question is exactly why I’m writing this article.

Because Solar and Fixed Deposits are NOT the same type of investment — and comparing them the wrong way can cost you lakhs.

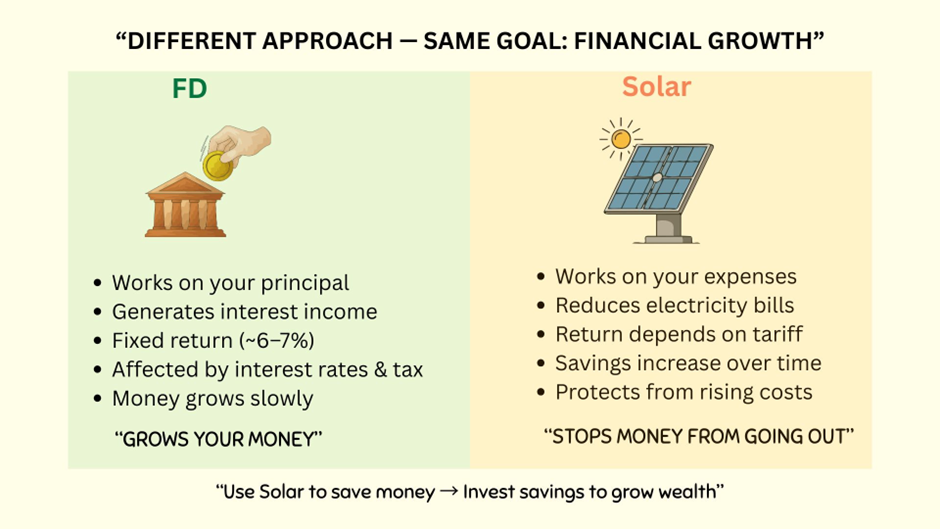

First, understand the Core Difference between Solar and FD

Most people compare Fixed Deposits and solar incorrectly. They assume both are similar types of investments.

But in reality, they work in completely different ways.

One creates money from your capital, while the other saves money by reducing your expenses.

A Fixed Deposit earns interest on your invested amount, whereas solar reduces your monthly electricity bill. In simple terms, a Fixed Deposit grows your money, while solar stops your money from going out.

There is a deeper way to understand this. A Fixed Deposit works on your principal, but solar works on your expenses. Because of this, they are not actually competing options — in many cases, they complement each other.

The money you save every month from solar can be reinvested into a Fixed Deposit or any other financial instrument. This way, solar doesn’t just save money; it can also indirectly help you grow your wealth.

Why This Matters Even More in India

Your electricity expense is not fixed. In fact, it is almost certain to increase over time.

This is mainly because a large portion of electricity in India is generated using coal. Coal is a limited, non-renewable resource, and as its cost increases, electricity tariffs also rise.

What this means in practical terms is simple. If your electricity bill is ₹5,000 today, it is very likely to be significantly higher in the next 5 to 10 years.

What Solar Really Does

Solar does not just reduce your electricity bill today. It effectively locks your electricity cost for the long term.

By installing solar, you protect yourself from rising tariffs and future price shocks. Instead of being affected by increasing electricity prices, you stabilize a major portion of your monthly expenses.

A Simple Way to think

A Fixed Deposit grows your money slowly over time. Solar, on the other hand, stops a growing expense.

One helps in building wealth, while the other helps in protecting it.

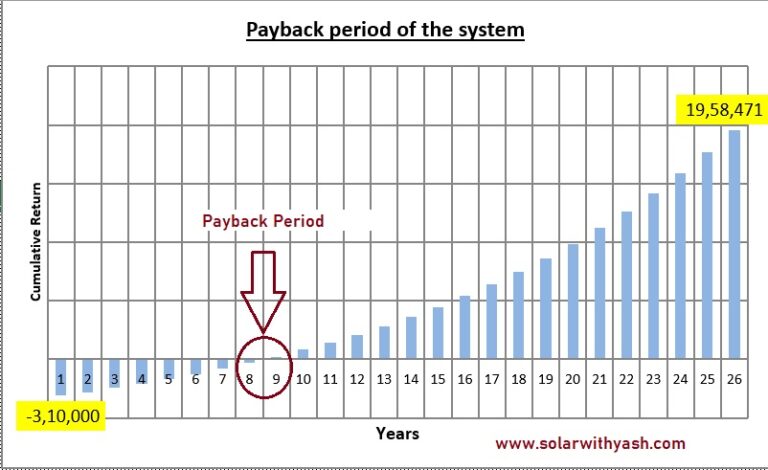

Solar Returns (Real Scenario)

Now let’s take the same ₹2.5 lakh and install solar.

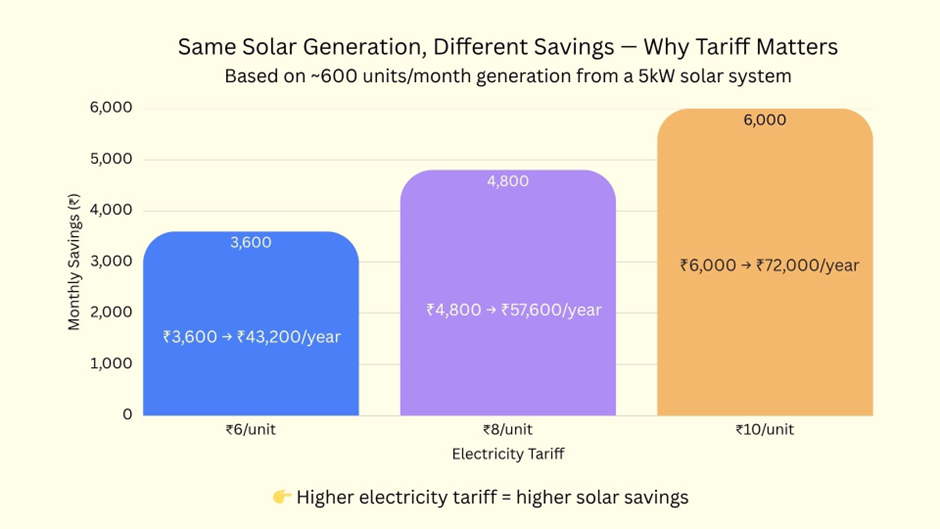

With this investment, you can typically install around a 5kW rooftop solar system. In most parts of India, such a system generates approximately 550–650 units per month, which averages to about 18–22 units per day.

For simplicity, let’s assume 600 units per month.

Now, your actual savings depend entirely on your electricity tariff.

This is also why different installers often give very different payback estimates. Learn more: “Why Two Installers Give Two Different Payback Periods.”

If your tariff is ₹6 per unit:

- Monthly savings ≈ ₹3,600 (₹6 × 600)

- Yearly savings ≈ ₹43,200

If your tariff is ₹8 per unit:

- Monthly savings ≈ ₹4,800

- Yearly savings ≈ ₹57,600

When it is ₹10 per unit:

- Monthly savings ≈ ₹6,000

- Yearly savings ≈ ₹72,000

So, in practical terms, your savings will typically fall in the range of ₹3,600 to ₹6,000 per month, depending on your tariff.

What Does This Mean as a Return?

Now let’s look at this from an investment perspective.

If you invest ₹2.5 lakh:

- At ₹43,200 yearly savings → return ≈ 17.3%

- At ₹72,000 yearly savings → return ≈ 28.8%

This means solar can realistically generate returns in the range of 17% to 28% annually, depending on your electricity cost.

To understand how these returns are actually calculated and what most people miss, read: “Simple Payback vs Real Payback in Solar: What Homeowners Must Know Before Investing”

Direct Comparison with Fixed Deposit

| Factor | Fixed Deposit | Solar |

|---|---|---|

| Investment | ₹2.5 lakh | ₹2.5 lakh |

| Yearly Return | ₹15,000–₹17,500 | ₹43,000–₹72,000 |

| Return % | ~6–7% | ~17–28% |

| Nature | Income generation | Expense reduction |

| Duration | Fixed | 20–25 years |

How Solar and FD Can Work Together

Instead of thinking in terms of “solar vs FD,” a better way to look at it is:

Solar + FD

The money you save every month from solar can be reinvested into a Fixed Deposit or other instruments.

For example:

- ₹4,000–₹6,000 monthly savings

- Can be invested regularly

Over time, this creates a compounding effect, where:

- Solar reduces your expenses

- FD (or other investments) grows your savings

This combination can accelerate your overall wealth creation much faster than using either option alone.

The Big Insight Most People Miss

Solar returns are not interest in the traditional sense. They are actually savings created by eliminating an expense.

Unlike Fixed Deposits, where returns depend on interest rates and are subject to taxation, solar savings come from reducing your electricity bill. This means your returns are not affected by bank rate changes, and there is no direct tax on the money you save.

Another important aspect that most people overlook is that these savings are not fixed — they are likely to increase over time.

As electricity tariffs rise in the future, your solar system will start replacing more expensive grid electricity. This means the value of each unit generated by your system increases, improving your effective returns over time.

In addition to financial benefits, solar also reduces your dependence on the grid. It moves you one step closer to energy independence, where you are less affected by external price fluctuations and supply uncertainties.

Recent global situations — including energy crises and rising fuel costs — have shown how dependent we are on limited energy resources. Over time, this dependency is expected to increase electricity costs further, making self-generation more relevant than ever.

There is also a psychological advantage that is often ignored. Knowing that your home is generating its own electricity creates a sense of control and confidence. It is not just about saving money — it is about becoming a more independent and future-ready homeowner.

But Is Solar Always Better?

No.

Let’s be honest — solar is not the right choice for everyone. Understanding where it fits (and where it doesn’t) helps you make a better decision.

Fixed Deposit is Better If:

- You need liquidity and quick access to your money

- You prefer zero risk and guaranteed returns

- You may need funds for other priorities in the near future

✅ Solar is Better If:

- Your monthly electricity bill is ₹3000 or higher

- You own your house and are not planning to relocate soon

- You are looking for long-term savings rather than short-term returns

In addition to this, a few practical factors also matter.

Your location should receive decent sunlight, which, fortunately, most parts of India do. The country receives strong solar radiation for most of the year, making rooftop solar viable in a majority of regions.

You should also have sufficient shadow-free rooftop space. Typically, a 1kW solar system requires around 60–70 sq. ft. of clean, unshaded area.

When these conditions are met, solar becomes not just a good option — but a highly effective long-term investment.

Not Sure If Solar is Right for You?

Instead of guessing, it’s always better to evaluate based on your own data.

If you want to check whether solar is feasible for your home, you can use the Solar Feasibility Spreadsheet. With a few basic inputs, it helps you:

- Estimate the right system size

- Calculate yearly savings based on your tariff

- Understand payback period

- Project 20–25year returns

- Evaluate key metrics like ROI, IRR, and NPV

This gives you a clear, numbers-based answer to the question:

👉 “Is solar actually worth it for me?”

Final Verdict: Solar vs Fixed Deposit

Let’s simplify everything.

If your primary goal is safety and liquidity, a Fixed Deposit remains a reliable option. It offers predictable returns and easy access to your money. However, if your goal is long-term financial efficiency and higher returns, solar stands out as a stronger choice.

The decision becomes clearer when you look at your electricity bill. If your monthly bill is below ₹2000, a Fixed Deposit may still be a better financial option. In the ₹3000 to ₹5000 range, it requires a more careful comparison. But if your bill is ₹5000 or higher, solar becomes a highly attractive investment due to the significant savings it can generate.

To understand this difference more clearly, consider two people investing the same ₹2.5 lakh. One chooses a Fixed Deposit and earns around ₹15,000 per year. The other installs solar and saves up to ₹96,000 per year. The initial investment is the same, but the outcomes are completely different.

This is why solar should not be seen as a simple yes-or-no decision. It is a numbers-based decision that depends on your electricity usage, tariff, and long-term plans.

If you want to understand what this looks like for your specific case, the best approach is to evaluate your own numbers. Based on your monthly electricity bill, you can estimate your system size, yearly savings, and actual payback period.

For those who want a more detailed and accurate analysis, a structured evaluation can provide clarity before investing. A proper financial breakdown helps you understand not just the payback, but also long-term returns over 20 to 25 years.

At a deeper level, there is no strict comparison between solar and Fixed Deposits. In reality, they complement each other. Solar reduces your expenses and creates consistent savings, while a Fixed Deposit can grow those savings over time. When used together, they not only improve financial returns but also move you closer to greater financial stability and energy independence as a homeowner.

In simple terms, a Fixed Deposit grows your money slowly, while solar stops your money from leaking every month.

Frequently Asked Questions

1. Is solar better than a fixed deposit in India?

Solar can offer higher effective returns than a fixed deposit because it reduces electricity expenses. While FDs typically give 6–7% returns, solar can provide 15–25% returns depending on your electricity tariff.

2. What is the ROI of a solar system in India?

The ROI of a rooftop solar system in India usually ranges between 15% to 28%, depending on electricity tariff, system size, and usage.

3. Is solar a safe investment like FD?

Solar is not identical to FD in terms of liquidity, but it is a low-risk investment as it reduces a recurring expense (electricity bills) for 20–25 years.

4. Can solar savings be invested further?

Yes, the money saved from reduced electricity bills can be reinvested into financial instruments like fixed deposits, mutual funds, or SIPs to grow wealth further.

5. Who should not invest in solar?

Solar may not be suitable for people who:

- Need immediate liquidity

- Have very low electricity bills

- Do not own their home