Payback vs IRR vs NPV — What Actually Matters for Solar Decisions

When homeowners try to evaluate a rooftop solar system, they are often introduced to multiple financial terms — payback, IRR, and sometimes NPV — without being clearly told what each number actually represents. This is why payback vs IRR vs NPV for solar creates so much confusion. Each metric answers a different question, but most quotations highlight only one, leaving homeowners with an incomplete financial picture.

When homeowners start exploring solar, the first number they hear is almost always the payback period.

“Your system will recover its cost in 5 years.”

“Payback is just 4.5 years.”

It sounds simple, reassuring, and decisive. Some installers go a step further and mention IRR (Internal Rate of Return) to make solar sound like a high-grade financial investment — similar to stocks, mutual funds, or real estate.

And NPV (Net Present Value)?

Almost nobody talks about it. As a result, most homeowners end up making long-term solar decisions using partial math, not wrong math — just incomplete.

I’ve reviewed dozens of real solar quotations where the payback looked excellent on paper, but when I analyzed the actual savings year by year, the financial reality told a very different story.

That confusion is exactly why this comparison matters.

- Payback tells how fast you recover money,

- IRR tells how efficiently money grows,

- NPV tells whether the project actually creates value over time.

Each metric answers a different question, and each also hides something important if used alone. That’s where confusion begins.

In this article, we’ll clearly break down:

(i) What Payback, IRR, and NPV really mean — in plain language

(ii) What each metric misses when used in isolation

(iii) And most importantly, which metric actually matters most for residential solar, and why

(iv) No sales talk.

(v) No finance-heavy theory.

(vi) Just practical clarity — so you can evaluate solar like a decision-maker, not a brochure reader.

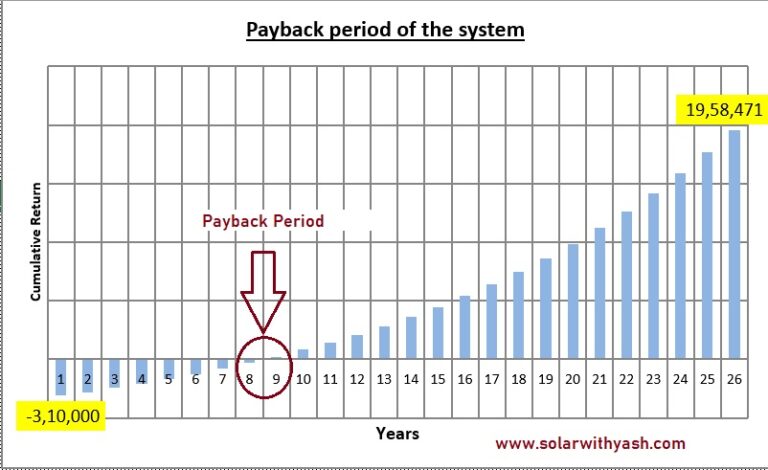

What Is Payback Period? (And Why Installers Love It)

The payback period is simply the time required for your solar savings to recover your initial investment.

Mathematically:

Payback = Total system cost ÷ Annual savings

Simple Example

(i) System cost: ₹2,50,000

(ii) Annual savings (Year 1): ₹50,000

So, Payback = 5 years

This means:

After 5 years, your total savings numerically match what you paid for the system.

That’s all payback tells you.

Why Payback Is So Popular (Especially in Solar Sales)

Payback is widely used because it is:

(i) Easy to understand

(ii) Quick to calculate

(iii) Easy to explain in one sentence

(iv) Psychologically comforting

(“After X years, electricity is free”)

For most homeowners, “When will I recover my money?” feels like the most natural question.

That’s why installers love payback.

The Hidden Assumptions Behind Payback.

Here’s the important part. Payback looks simple, but it quietly assumes many things that are not true in the real world.

Let’s break them down.

1️⃣ It Uses First-Year Savings (Which Are Inflated)

Payback usually uses Year-1 savings.

But in the first year:

(i) Maintenance cost is almost zero

(ii) Panels are brand new

(iii) No inverter aging

(iv) No cleaning issues yet

So, Year-1 savings are the best-case savings, not the average savings.

Example:

(i) Year-1 savings: ₹50,000

(ii) Average real savings over 25 years: lower

Payback locks in this optimistic number forever.

2️⃣ It Assumes Savings Stay Constant Every Year

Payback assumes: “If you saved ₹50,000 this year, you’ll save ₹50,000 every year.”

But in reality:

(i) Panel output degrades

(ii) Maintenance costs increase slowly

(iii) Inverter replacement may happen

(iv) Grid tariff escalation may differ from assumptions

Real savings change every year — they are not flat.

Payback ignores this completely.

3️⃣ It Ignores the Time Value of Money

This is a big one.

Payback treats: ₹50,000 saved today and ₹50,000 saved 15 years later as equal.

But they are not.

Money today:

(i) Can earn interest

(ii) Can be invested

(iii) Has a higher real value

Payback does not discount future savings at all.

4️⃣ It Completely Ignores Savings After Payback

Suppose:

(i) System life = 25 years

(ii) Payback = 5 years

That means: The system’s life beyond the 5th year is ignored

Payback does not care whether:

(i) You save ₹10,00,000 after payback

(ii) Or ₹20,00,000 after payback

Both look the same in payback terms.

5️⃣ It Ignores Financing Cost

If the system is financed:

(i) Interest increases the total cost

(ii) EMIs change cash flow timing

But payback usually assumes:

(i) “Cash purchase.”

(ii) “Or silently ignores interest.”

This can make financed solar look much better than it really is.

📌 Key Insight (Most Important)

Payback answers only one question:

“When do I break even numerically?”

It does not answer:

(i) Is this a good financial decision?

(ii) Is my money growing efficiently?

(iii) Am I better off investing elsewhere?

(iv) How much value does solar create over its lifetime?

Payback is a starting point, not a decision tool. That’s why, for serious solar decisions, payback alone is incomplete math.

What Is IRR? (Why It Sounds Smart but Can Mislead)

What IRR Really Means

IRR (Internal Rate of Return) is the annualized return your solar investment appears to generate over its lifetime.

In simple words, IRR tells you how efficiently your invested money grows per year, on average.

That’s why IRR is often compared with:

(i) Fixed Deposits (FD)

(ii) Bonds

(iii) Mutual funds

(iv) Other long-term investments

A Realistic Indian Example (₹)

Let’s take a typical Indian residential case:

(i) Solar system cost: ₹2,50,000

(ii) System size: 5 kW

(iii) Year-1 savings: ₹50,000

(iv) System life: 25 years

(v) Savings increase slowly as electricity tariffs rise

(vi) Panel output slowly degrades over time

When all these yearly cash flows are put into an IRR calculation, the result often comes out to:

IRR ≈ 12–14%

On paper, this looks excellent. It makes solar appear:

(i) Better than FD

(ii) “Comparable to long-term equity returns like a “high-return investment.”

This is why IRR is heavily used in solar quotations.

Why IRR Looks Very Attractive

IRR feels convincing because:

✅ It gives one clean percentage

✅ It sounds financially sophisticated

✅ It allows easy comparison (“Solar gives 12%, FD gives 6%”)

✅ It positions solar as an investment product, not an expense

But this neat percentage hides important realities.

The Hidden Problems with IRR: IRR is not wrong, but it is easy to misinterpret, especially for homeowners.

1️⃣ IRR Assumes Reinvestment at the Same IRR (Unrealistic)

This is the biggest issue.

IRR assumes that: Every rupee you save from solar is reinvested at the same IRR.

Example:

(i) Annual savings: ₹50,000

(ii) IRR shown: 12%

IRR math assumes that ₹50,000 is reinvested every year at 12%, consistently, for 25 years

But in real life:

(i) You use that money for household expenses

(ii) Or it simply reduces your electricity bill

(iii) Or it sits in a savings account

You do not reinvest solar savings at a rate of 12% every year. Therefore, the IRR becomes theoretical rather than practical.

2️⃣ IRR Is Extremely Sensitive to Assumptions

Small changes in assumptions can change the IRR a lot.

For the same 5 kW system:

(i) Tariff escalation: 3% vs 6%

(ii) Degradation: 0.5% vs 0.8%

(iii) System life: 20 vs 25 years

(iv) Inverter replacement timing

(v) Financing vs full cash

Result: IRR can swing from 10% to 15% without changing the system itself. IRR looks precise, but it is fragile.

3️⃣ Two Systems Can Have the Same IRR but Very Different Savings

Example:

| System | IRR | Lifetime Savings |

|---|---|---|

| System A | 12% | ₹7 lakh |

| System B | 12% | ₹12 lakh |

Same IRR but very different actual money saved.

IRR does not tell you:

(i) How much cash solar puts in your pocket

(ii) How much cheaper is solar electricity than grid power

Key Insight

IRR answers: “What is the implied annual return rate of this project?”

It does not answer:

(i) How much money you actually save over 25 years

(ii) Whether solar beats grid electricity in total cost

(iii) Whether this is a good long-term household decision

IRR sounds smart. However, it does not reveal the full financial truth of solar energy by itself.

“IRR works best for projects where cash flows are actually reinvested — which is rarely the case for household electricity savings.”

What Is NPV? (The Metric That Actually Tells the Truth)

What NPV Really Means: NPV (Net Present Value) tells you how much money you truly gain or lose by going solar — after accounting for time.

“NPV measures value, not speed.”

In simple words:

NPV = Today’s value of all future solar savings − money you invest today

Unlike payback or IRR, NPV does not compress everything into one time or one percentage.

It converts every future saving into today’s rupees and then adds them up.

Why “Today’s Value” Matters (Indian Context):

₹1 saved today is more valuable than ₹1 saved 10 years later.

Why?

Because:

(i) Money has an opportunity cost

(ii) Inflation reduces future purchasing power

(iii) You could invest today’s money elsewhere

Example (very simple):

₹10,000 today vs ₹10,000 after 10 years. Even if the number is the same, the real value is not.

This is why NPV uses a discount rate.

What Is Discount Rate? (Simple Indian Example)

A discount rate answers this question:

“What return do I expect from a safe alternative if I don’t go solar?”

In India, typical discount rates used are:

(i) 6–7% → long-term FD / government bond range

(ii) 8–10% → conservative household expectation

Example: You expect 7% return from a safe alternative. Therefore, future solar savings are discounted at 7% to convert them into their present value.

This makes the comparison fair and realistic.

Simple Indian Example (₹)

Let’s take a realistic case:

(i) System size: 5 kW

(ii) Cost today: ₹2,50,000

(iii) Year-1 savings: ₹50,000

(iv) System life: 25 years

(v) Discount rate: 7%

(vi) Degradation and maintenance included

When all future yearly savings are discounted back to today and added together:

(i) Present value of all savings ≈ ₹3,30,000

(ii) Initial investment = ₹2,50,000

So, NPV = ₹3,30,000 − ₹2,50,000 = +₹80,000

How to Read This Result

(i) NPV > 0 → Solar is financially attractive

(ii) NPV = 0 → Solar just breaks even

(iii) NPV < 0 → Solar is financially unattractive

In this case, Solar makes you ₹80,000 richer in today’s money, even after accounting for time and risk. That is real value — not a marketing number.

Why NPV Is Superior for Residential Solar

NPV is powerful because it:

✅ Shows absolute money gained

✅ Penalizes delayed or back-loaded savings

✅ Naturally includes: Degradation, Maintenance, Tariff escalation, and Inverter replacement

✅ Works equally well for: Cash purchase, Loan-based solar, and Partial debt + equity scenarios

Payback and IRR struggle with these realities. But NPV handles them cleanly.

📌Key Insight

NPV answers the only question that truly matters:

“Am I actually richer after going solar?”

If the answer is yes — solar makes financial sense.

If not — no amount of short payback or high IRR can fix that.

Same Solar System — Three Metrics, Three Stories

Now let’s see how the same solar system can tell three very different stories, depending on the metric used.

Example (USA):

(i) System cost: $18,000

(ii) Annual savings (Year-1): $1,400

(iii) System life: 25 years

(iv) Discount rate: 6–7%

Results:

(i) Payback ≈ 13 years

(ii) IRR ≈ 7–8%

(iii) NPV ≈ +$6,500

What Each Metric Says:

(i) Payback says: “Hmm… 13 years feels long.”

(ii) NPV says: “This system adds $6,500 of real value in today’s money.”

(iii) IRR says: “Okay… average investment return.”

Same system.

Same cash flows.

Three completely different conclusions.

“The logic is identical in India, and the U.S. — only tariffs, discount rates, and incentives change.”

📌 Observation (Very Important)

Payback focuses only on when money returns

IRR focuses only on rate, not amount

NPV focuses on the total value created

That’s why professionals trust NPV — and homeowners should too.

“If you want to calculate Payback, IRR, and NPV for your own home using realistic assumptions (tariffs, losses, degradation, financing), you can use the Solar Feasibility Spreadsheet (SFS): India Edition and US Edition. It shows all three metrics together — so you don’t rely on one misleading number.”

Which Metric Should Homeowners Focus On?

| Metric | Usefulness | Verdict |

|---|---|---|

| Payback | Quick sanity check | ❌ Incomplete |

| IRR | Comparison tool | ⚠️ Context-dependent |

| NPV | Decision metric | ✅ Most important |

📌 Rule of thumb:

(i) Use payback to understand the timeline

(ii) Use IRR to compare alternatives

(iii) Decide using NPV

Why Most Solar Calculators Get This Wrong

Most online solar calculators give optimistic results because they simplify the math too aggressively. Many of them ignore discounting altogether, treating ₹1 saved today and ₹1 saved 15 years later as equal.

Some assume unrealistically high grid tariff escalation, which inflates future savings on paper but rarely holds in reality. Others quietly hide system losses, degradation, and inverter replacements, making first-year performance look permanent.

Another common mistake is mixing financing with feasibility — loan EMIs are treated as project performance, which distorts the true economics of solar itself. This is why real-world payback often ends up being 2–3 years longer than what calculators promise, something I’ve explained in detail here: Why Solar Payback Calculations Are Wrong by 2–3 Years.

How to Evaluate Solar Properly (Without Being a Finance Expert)

To judge a solar system correctly, you don’t need complex finance knowledge—you just need to look at the right signals. Focus on year-by-year cash flows instead of headline numbers, check the discounted break-even year rather than simple payback, and always look at total lifetime net savings to understand the real outcome.

Avoid making decisions based on a single number, and be especially cautious of marketing-driven IRR figures shown without assumptions. A proper solar feasibility analysis evaluates payback, IRR, and NPV together, using realistic tariffs, losses, degradation, and financing assumptions—the same disciplined approach used by solar consultants and financial analysts.

Conclusion: Payback Is a Shortcut — NPV Is the Truth

Payback is not wrong—it simply answers a limited question. IRR is also not useless—it tells you how efficiently money grows. But neither of them tells the full story on its own.

For residential solar, the real decision should be driven by NPV, because it shows the actual financial outcome after considering time, risk, and real cash flows. If the NPV is positive and the assumptions used are realistic, solar is not just emotionally satisfying or environmentally good—it financially makes sense. In the end, solar should not just pay back your money; it should leave you better off.

Frequently Asked Questions

1. Is the payback period enough to decide whether solar is worth it?

No. Payback only tells you when you recover your initial cost. It does not show how much money you actually gain over the system’s lifetime.

2. Why do installers focus so much on payback?

Because it is easy to explain and sounds reassuring. However, it ignores factors like time value of money, degradation, and long-term savings.

3. Is IRR a good metric for residential solar?

IRR can be useful, but it is often misunderstood. A high IRR does not always mean higher total savings, and it depends heavily on assumptions.

4. What does NPV tell me that payback and IRR don’t?

NPV tells you the actual financial benefit of going solar after accounting for time, risk, and realistic cash flows. It answers: Will I truly be better off financially?

5. What discount rate should homeowners use for NPV?

A reasonable discount rate is usually close to long-term inflation, fixed deposit rates, or government bond yields (typically 6–8% in India, 5–7% in the U.S.).

6. Can a solar system have a long payback but still be a good investment?

Yes. Many solar systems have long payback periods but still generate strong lifetime savings and positive NPV.

7. Should I compare solar IRR with mutual funds or stocks?

Not directly. Solar is a cost-saving asset, not a market investment. The risk profile and cash flow nature are completely different.

8. Which metric should I trust the most?

Use all three—but make the final decision based on NPV, using realistic assumptions.

🔗 Free tool: Download my Solar Snap tool to quickly estimate solar potential at your home